Reflecting on Greenwich's substantial involvement in the creation and development of the worlds telecommunication network that we all take for granted today, as well as the impacts of rapid fibre expansion and what it means for businesses.

This article was first published in Masthead (the SE London Chamber of Commerce magazine) in January 2026. It's reproduced here for the convenience of our readers, but you can also check out the full online edition of the magazine.

I find it remarkable how much my home area of SE London has shaped the world. For 140 years, Greenwich has been central to time (Greenwich Mean Time) and location (the Prime Meridian). What's less obvious is that the area has also played a pivotal role in telecommunications.

Towns across Britain used to have different local times derived from sundials. The rise of the railways led to needing a single uniform timetable, so in 1847, Greenwich Time was adopted nationwide. Five years later, the first telegraph-linked clock was installed at Lewisham station, synchronised to the Royal Observatory, providing the blueprint for all railway timekeeping.

As the telegraph network grew, cable production expanded among companies on the Greenwich Peninsula. Circa 1860, they twice manufactured subsea cables for transatlantic telegraphs, loaded onto ships using gantries like the one preserved at Enderby Wharf, now a scheduled monument as of October 2025. Messages that once took weeks crossed the Atlantic in minutes, transforming global communication.

By 1954, telegraphs had mostly given way to voice calls, with Submarine Cables Ltd manufacturing the first transatlantic telephone cable at factories in Greenwich, Woolwich and Erith. In 1970 they were acquired by Standard Telephones and Cables, who became the sole UK manufacturer of undersea cables. Working for STC was Charles Kao, a former Woolwich Polytechnic student, who pioneered practical fibre-optic technology (for which he received the Nobel Prize in Physics in 2009). In 1988, the first transatlantic fibre-optic cable was laid, also partly made by STC. The Greenwich site is today occupied by Alcatel Submarine Networks, continuing the legacy.

Yet domestic broadband lagged behind, remaining on ageing telephone wires and dial-up modems until "Fibre to the Cabinet" (FTTC) was introduced in 2010 to bring fibre closer to customers. Although improved, it still relied on old telephone wires into the premises, so performance was variable and speeds handicapped. Despite not being wholly accurate, regulators also permitted use of the term "fibre" in marketing, which has created lasting confusion.

The equipment used to operate the analogue telephone network is no longer being supported. BT Openreach announced its closure in 2017, with the industry's final target for migrating customers being January 2027. This is the landline equivalent of the 2012 analogue TV switch-off.

This matters for businesses because landline phones, alarms, lifts and services that relied on analogue now need to operate over an Internet-only digital connection, which requires planning and forethought. Voice services need to be migrated to what is called "Voice over IP", more colloquially known as "digital voice".

Although copper telephone cables may remain to support broadband for years to come, the ultimate goal is to migrate everyone to a "full fibre" data connection, which is 100% fibre optic all the way into the home or business. Whilst most users won't need the extreme speeds advertised today, the technology is future-proofed and far more reliable.

Full fibre isn't yet available everywhere, leaving underserved pockets of the country including many parts of Greenwich and SE London. That has allowed new network builders to step in, such as the council-backed initiative "Digital Greenwich Connect", which partners with Enlink to bring full fibre to local businesses.

Known informally as "altnets", these alternative network builders expanded rapidly after Ofcom mandated open access to Openreach's ducts and poles. The result was a circa-2020 investment boom and a "gold rush" of rapid builds and heavy competition. This created a race to build infrastructure and acquire customers. In some cases, this has led to lower-quality deployments, prioritising faster rollout over long-term reliability. And whilst competition benefits customers, having too many physical networks competing for the same premises is unsustainable; many altnets will struggle to remain viable.

Aggressive deals have been used to win new subscribers, which in turn has conditioned customers to expect more for less at every renewal. Whilst it is historically true that bandwidth prices have reduced year-on-year, recently this effect has bottomed out, being offset by inflation and the rising costs of build, maintenance and financing.

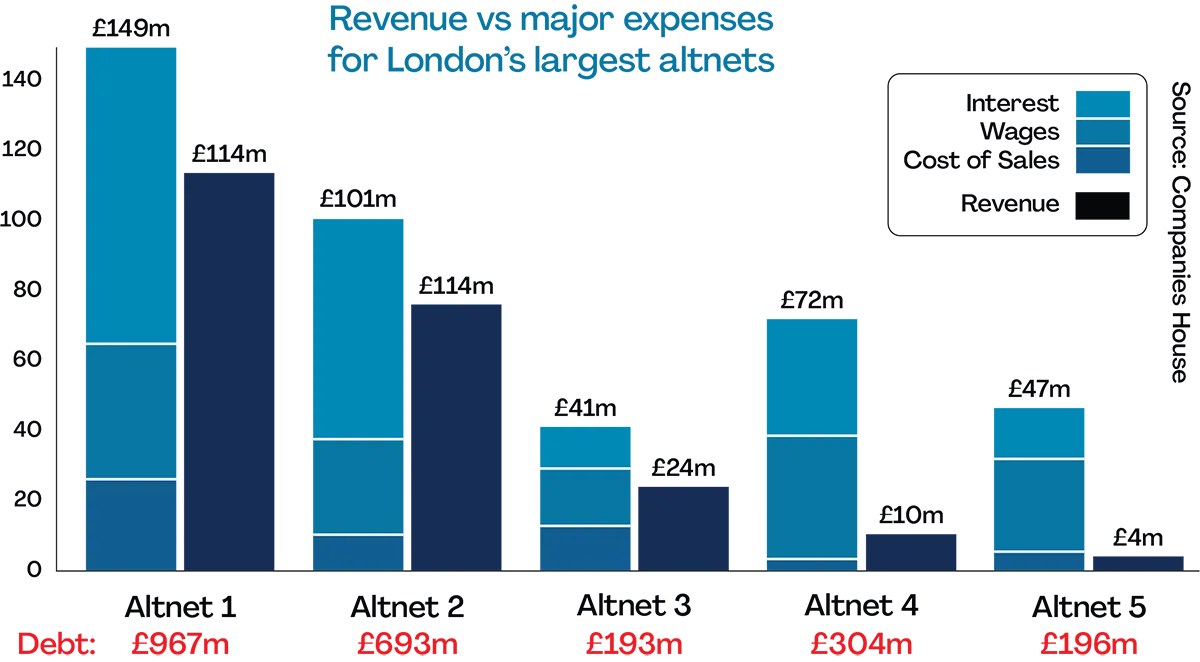

This imbalance is reflected in the sector's finances: none of the five largest London alternative network operators have sufficient revenues to cover operating, staffing, and interest costs; and the capital debts average 10x revenues.

This puts all UK telecommunications under pressure, just when connectivity is becoming ever more vital with the analogue switch-off, hybrid working, smart everything and AI assistants. Telecoms has long been known for its large providers having poor outsourced customer service and a tendency to underinvest; this won't improve in the race-to-bottom price war.

[Author's note: just before going to press, G.Network (one of the five cited examples) sold to distressed debt specialist FitzWalter Capital and promptly entered administration, confirming the mounting financial pressures]

Until the current "fibre bubble" bursts, there remains artificially low pricing as investors demand customer uptake at any costs.

Many of the altnets won't survive as the market corrects; those that do will form a critical utility and must be built for the long term to ensure the UK has a stable and reliable infrastructure. At Enlink, we prioritise certainty and resilience over immediate cost; avoiding the pitfalls of the adage "buy cheap, buy twice".

With echoes from history, it is inevitable that there will be consolidation similar to UK cable TV in the 1990s, which produced Virgin Media as the only national fixed-line operator alongside BT. This time we could end up with a third national fibre optic player, similar to how consolidation of Vodafone and Three in the mobile sector has left three national cellular networks.

For businesses, connectivity is a critical utility, underpinning phones, payments, cloud services and day-to-day operations. No internet means no productivity. When choosing a provider, it's worth looking beyond headline speeds and prices to ask how the network is built, who it's built for, and how quickly real people can help if something goes wrong.

These details make the difference between a connection that just looks good in the advertising, and one you can actually rely on.

If you have questions about getting your business connected, contact us today, or visit our homepage for more information.